U.S. Positron Emission Tomography Market Analysis by Product Type & Application 2026–34

United States Positron Emission Tomography Market Size and Forecast 2026–2034

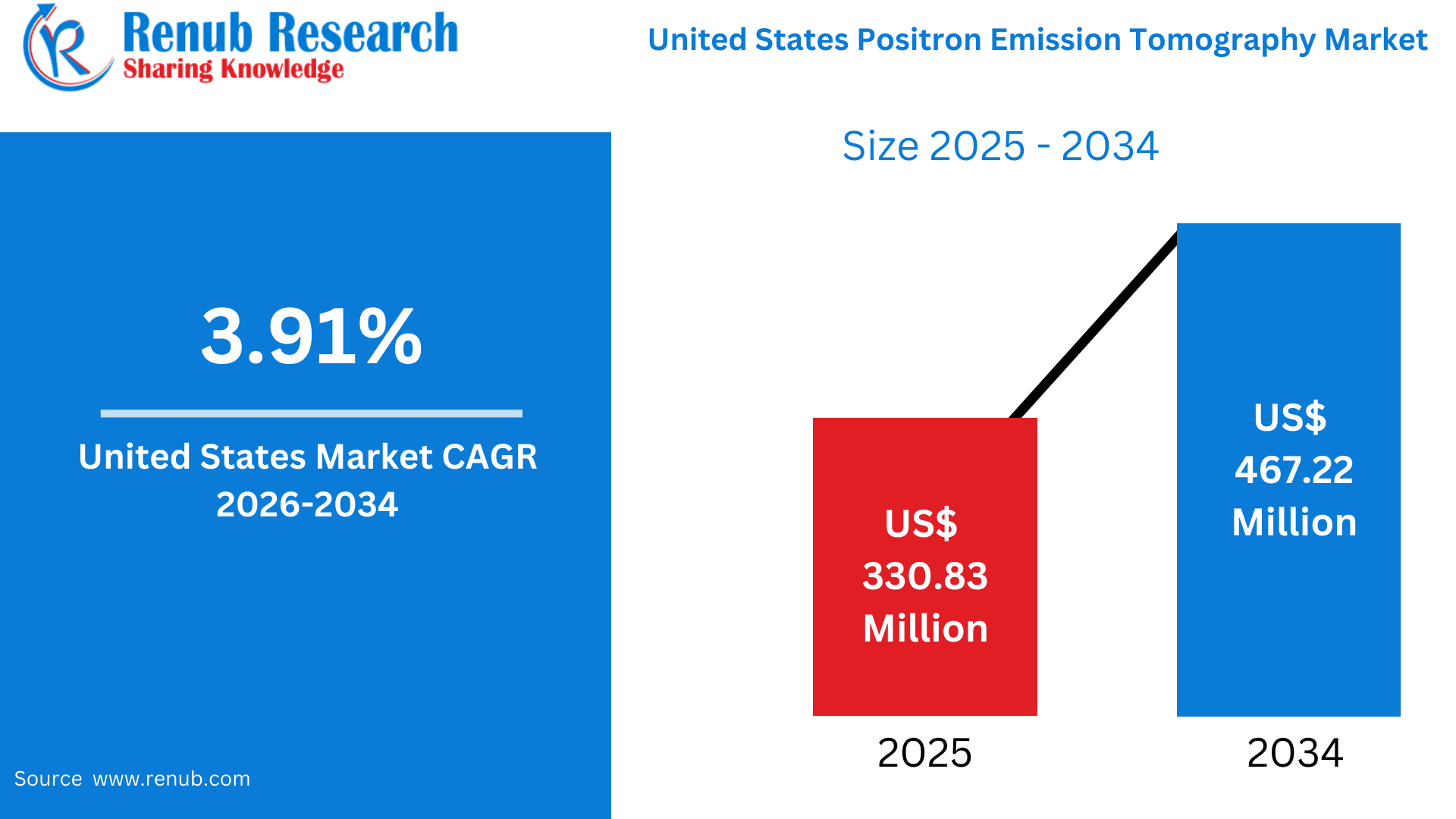

According to Renub Research United States Positron Emission Tomography (PET) market is projected to experience steady and sustainable growth over the forecast period, expanding from US$ 330.83 million in 2025 to US$ 467.22 million by 2034, at a compound annual growth rate (CAGR) of 3.91% from 2026 to 2034. This growth is primarily supported by the rising prevalence of chronic and life-threatening diseases, continuous technological advancements in PET scanner systems, and increasing demand for early, precise, and non-invasive diagnostic solutions across healthcare facilities. PET imaging has become a critical pillar of modern diagnostic medicine in the United States, particularly in oncology, cardiology, and neurology, where functional and metabolic insights are essential for clinical decision-making.

Download Free Sample Report:https://www.renub.com/request-sample-page.php?gturl=united-states-positron-emission-tomography-market-p.php

United States Positron Emission Tomography Market Outlook

Positron Emission Tomography is an advanced nuclear imaging technology designed to visualize biochemical and physiological processes occurring within the human body. The procedure involves administering a small amount of a radiopharmaceutical compound, which emits positrons as it decays. When these positrons interact with electrons in the body, gamma rays are released and captured by detectors within the PET scanner. These signals are reconstructed into detailed three-dimensional images that represent metabolic activity at the cellular level.

Unlike conventional imaging techniques that focus on anatomical structures, PET imaging excels in detecting functional abnormalities before structural changes occur. This capability makes PET particularly valuable for early disease detection, accurate staging, treatment planning, and therapy monitoring. In the United States, PET imaging has become deeply embedded in clinical practice due to its effectiveness in managing cancer, neurological disorders, and cardiovascular diseases. The widespread integration of hybrid systems such as PET/CT and PET/MRI has further enhanced diagnostic accuracy, reinforcing PET’s importance within the country’s advanced healthcare infrastructure.

Increasing Incidence of Cancer and Chronic Diseases

The rising incidence of cancer, cardiovascular disease, and neurological disorders is one of the most influential growth drivers for the United States PET market. PET imaging plays a central role across the cancer care continuum, including tumor detection, staging, treatment response evaluation, and recurrence monitoring. As cancer prevalence continues to rise, PET has become indispensable for oncologists seeking to deliver personalized and targeted treatment strategies.

Chronic diseases remain a significant public health burden in the United States, with a large proportion of the population affected by conditions such as heart disease, diabetes, obesity, and neurodegenerative disorders. PET imaging supports early and precise diagnosis of these conditions by revealing metabolic dysfunctions that may not be visible through traditional imaging methods. As healthcare systems increasingly emphasize preventive care and early intervention, PET imaging continues to gain traction in hospitals and diagnostic centers nationwide.

Technological Advancements and Hybrid Imaging Evolution

Technological progress has significantly accelerated the adoption of PET imaging in the United States. Hybrid imaging platforms such as PET/CT and PET/MRI combine metabolic information with high-resolution anatomical detail, providing superior diagnostic confidence compared to standalone PET systems. These hybrid modalities are particularly valuable in oncology, neurology, and cardiology, where precise localization of disease is critical.

Advancements in detector materials, digital PET technology, and time-of-flight imaging have further improved image resolution while reducing radiation dose and scan duration. Simultaneously, innovation in radiopharmaceutical development has expanded PET’s clinical applications, enabling more accurate imaging of neurological, cardiac, and metabolic disorders. The growing field of theranostics, which integrates PET imaging with targeted radiopharmaceutical therapy, is expected to further drive innovation and adoption in the U.S. PET market.

Expansion of Diagnostic Centers and Reimbursement Support

The expansion of freestanding diagnostic imaging centers has played a crucial role in driving PET market growth in the United States. These centers improve patient access to advanced imaging services, reduce wait times, and support higher imaging volumes outside of traditional hospital settings. Dedicated PET centers often focus on operational efficiency, image quality, and rapid scheduling, making them attractive to both referring physicians and patients.

Reimbursement support has also strengthened PET adoption. Favorable reimbursement policies for PET procedures, especially in oncology and cardiology, enhance the economic viability of PET imaging for providers. As insurance providers increasingly recognize PET’s role in improving diagnostic accuracy and reducing long-term healthcare costs, reimbursement coverage continues to expand. This financial support encourages healthcare facilities to invest in PET infrastructure and advanced imaging technologies.

Equipment Cost and Operational Challenges

Despite its clinical benefits, PET imaging faces notable challenges related to high equipment and operational costs. Advanced PET systems, particularly PET/CT and PET/MRI scanners, require substantial capital investment, along with specialized infrastructure and radiation shielding. These costs can limit adoption among smaller hospitals, rural healthcare facilities, and independent clinics.

Operational expenses further add to the financial burden, including radiopharmaceutical procurement, personnel training, regulatory compliance, and ongoing maintenance. As a result, PET services are often concentrated in large hospitals, academic medical centers, and high-volume diagnostic facilities. While technological advancements are gradually improving cost efficiency, financial barriers remain a key constraint to broader market penetration.

Radiotracer Supply Constraints and Regulatory Complexity

PET imaging relies on radiotracers with short half-lives, requiring reliable and timely production and distribution. Limited availability of cyclotron facilities in certain regions can disrupt supply chains, leading to scheduling delays and reduced scanner utilization. Logistical challenges related to transportation and handling of radioactive materials further complicate radiotracer availability.

The regulatory environment governing radiopharmaceutical development and use is stringent, with lengthy approval processes for new tracers. While these regulations ensure safety and quality, they can slow innovation and market entry. As PET applications expand into neurology, cardiology, and theranostics, ensuring consistent access to diverse radiotracers remains a critical challenge for the U.S. PET market.

United States Full-Ring PET Scanners Market

Full-ring PET scanners dominate the United States market due to their superior sensitivity, enhanced image resolution, and faster acquisition times. These systems feature a continuous ring of detectors that capture a higher proportion of emitted photons, resulting in more accurate metabolic imaging. Full-ring scanners are widely deployed in hospitals, cancer centers, and high-volume diagnostic facilities.

Their precision and reproducibility are particularly valuable in oncology, where accurate assessment of tumor metabolism directly influences treatment decisions. Integration with time-of-flight technology, digital detectors, and AI-driven image reconstruction has further strengthened the clinical value of full-ring PET scanners. Despite higher capital costs, their diagnostic accuracy and operational efficiency justify widespread adoption, ensuring their continued dominance in the U.S. PET market.

United States Bismuth Germanium Oxide PET Market

Bismuth Germanium Oxide (BGO)-based PET scanners maintain a stable presence in the U.S. market due to their cost-effectiveness and reliable performance. BGO crystals offer high stopping power for gamma photons, making them suitable for conventional PET imaging, particularly in oncology applications where ultra-high temporal resolution is not critical.

These systems are often favored by budget-conscious diagnostic centers and community hospitals seeking dependable imaging solutions. Although newer detector materials such as LYSO and LFS provide faster response times, BGO remains relevant due to its durability, proven track record, and favorable price-to-performance ratio. As demand grows in mid-sized and regional healthcare facilities, BGO-based PET scanners continue to hold a steady market share.

United States Lutetium Fine Silicate PET Market

Lutetium Fine Silicate (LFS) detectors represent a next-generation advancement in PET imaging technology. LFS offers high light output and fast decay times, enabling improved time-of-flight performance and superior image clarity. In the United States, LFS-based PET scanners are increasingly adopted by advanced diagnostic centers and research institutions focused on precision imaging.

These detectors support lower radiation doses and shorter scan times, improving patient comfort and operational throughput. LFS technology is particularly valuable for detecting small lesions and supporting sophisticated neurological and cardiac imaging studies. Although LFS systems are more expensive than older crystal technologies, their clinical advantages align with the industry’s shift toward higher diagnostic accuracy and precision medicine.

United States Cardiology PET Market

PET imaging is playing an increasingly important role in cardiology across the United States. Compared to traditional SPECT imaging, PET offers superior diagnostic accuracy in evaluating myocardial perfusion, blood flow, and metabolic activity. This capability is critical for detecting coronary artery disease, assessing ischemia, and guiding interventional strategies.

As cardiovascular disease remains a leading cause of morbidity and mortality, cardiologists are increasingly relying on PET to enhance diagnosis and risk stratification. The ability to quantify myocardial blood flow provides valuable insights for personalized treatment planning. Advances in cardiac-specific radiotracers further strengthen PET’s role, positioning cardiology as one of the fastest-growing application segments in the U.S. PET market.

United States Neurology PET Market

The neurology segment of the U.S. PET market is experiencing rapid growth due to the rising prevalence of neurodegenerative disorders such as Alzheimer’s disease, Parkinson’s disease, and epilepsy. PET imaging enables early detection of metabolic and molecular changes in the brain, often years before structural abnormalities become visible through conventional imaging.

The development of novel tracers targeting amyloid plaques, tau proteins, and dopamine transporters has significantly enhanced diagnostic specificity. PET supports precision medicine approaches by helping neurologists assess disease progression and therapeutic response. Growing public awareness of brain health, coupled with an aging population and expanding neurotherapeutic research, is expected to sustain long-term growth in this segment.

United States PET Diagnostic Centers Market

Diagnostic imaging centers serve as a major growth engine for the U.S. PET market by providing accessible, specialized imaging services outside hospital networks. These centers enable high patient throughput, competitive pricing, and operational specialization. Early adopters of hybrid PET systems, diagnostic centers focus on imaging quality, rapid turnaround times, and strong physician referral networks.

Geographic distribution of diagnostic centers improves access in suburban and rural areas where hospital PET departments may be limited. Many centers establish long-term agreements with radiopharmaceutical suppliers to ensure consistent tracer availability. As value-based healthcare models emphasize efficiency and cost control, outpatient PET centers are expected to capture an increasing share of imaging volumes.

California Positron Emission Tomography Market

California represents one of the most advanced PET imaging markets in the United States, supported by world-class healthcare systems, leading research institutions, and a high concentration of cancer centers. Strong demand exists for oncology and neurology PET imaging, reinforced by robust referral networks and clinical research activity.

The state is an early adopter of digital PET and hybrid PET/MRI technologies, benefiting from its strong biomedical innovation ecosystem. Despite high operational costs, favorable reimbursement structures and large patient volumes sustain ongoing market expansion, positioning California as a key driver of national PET technology adoption.

New York, Texas, and Arizona Positron Emission Tomography Markets

New York’s PET market is anchored by major academic medical centers, specialized cancer facilities, and dense urban populations. High screening rates, strong physician networks, and early adoption of advanced imaging technologies drive consistent demand across oncology, neurology, and cardiology.

Texas is among the fastest-growing PET markets due to population growth, expanding healthcare networks, and relatively lower operational costs. Increased investments in diagnostic centers and tracer supply infrastructure support market expansion across both urban and suburban regions.

Arizona’s PET market is steadily growing, driven by an aging population, rising chronic disease prevalence, and expanding healthcare infrastructure. Improvements in cyclotron networks and increased insurance coverage continue to enhance PET accessibility across the state.

Competitive Landscape and Key Market Participants

The United States PET market is characterized by strong competition among global imaging technology providers and specialized manufacturers. Leading companies include GE Healthcare, Siemens Healthineers AG, Koninklijke Philips NV, Hitachi Ltd., Mediso Medical Imaging Systems Ltd., and Neusoft Medical Systems.

These companies compete through continuous innovation, system upgrades, and strategic partnerships, focusing on improving image quality, workflow efficiency, and clinical outcomes. As demand for early and accurate diagnosis continues to rise, the United States Positron Emission Tomography market is expected to maintain stable and sustained growth through 2034.