Europe Direct Drive Wind Turbine Market Analysis and Forecast 2025–2033

Europe Direct Drive Wind Turbine Market Size and Forecast (2025–2033)

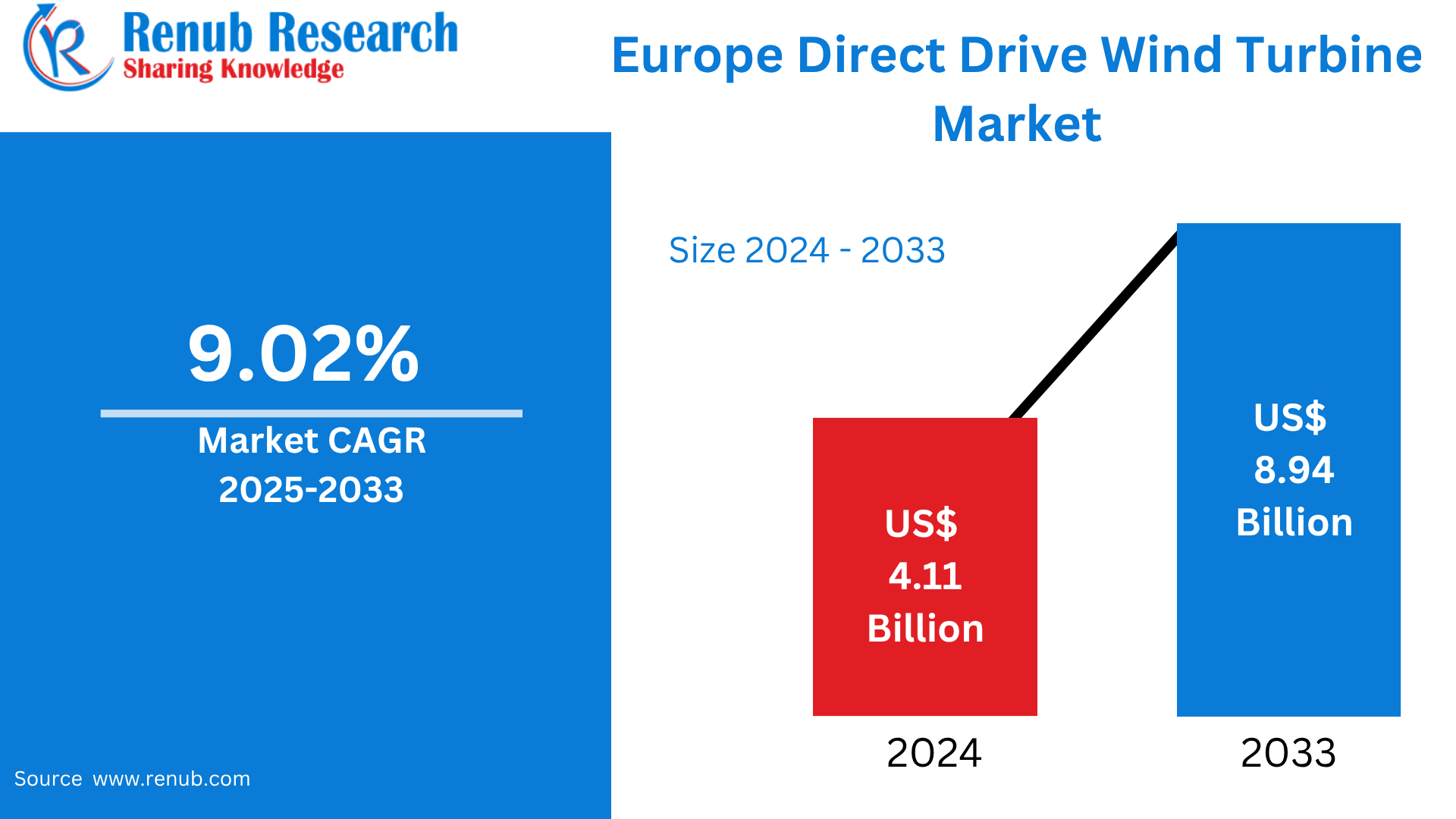

According To Renub Research Europe direct drive wind turbine market is entering a phase of accelerated growth as the region intensifies its transition toward clean and sustainable energy systems. Valued at approximately US$ 4.11 billion in 2024, the market is projected to reach around US$ 8.94 billion by 2033, registering a strong compound annual growth rate (CAGR) of 9.02% during the forecast period from 2025 to 2033. This robust expansion is primarily driven by rising investments in renewable energy infrastructure, supportive government policies, and increasing preference for low-maintenance, high-efficiency wind turbine technologies. As Europe works toward ambitious decarbonization and energy security targets, direct drive wind turbines are emerging as a critical technology choice across both onshore and offshore applications.

Europe Direct Drive Wind Turbine Market Overview

A direct drive wind turbine is an advanced wind energy system that eliminates the traditional gearbox, connecting the turbine rotor directly to a low-speed generator. The removal of the gearbox—one of the most failure-prone and maintenance-intensive components in conventional turbines—results in enhanced reliability, reduced operational costs, and longer equipment lifespan. These advantages make direct drive turbines especially suitable for large-scale and offshore wind installations, where maintenance access is limited and downtime is costly.

Europe has been at the forefront of wind energy adoption for decades, and the shift toward direct drive technology reflects the region’s focus on innovation, efficiency, and long-term sustainability. Countries such as Germany, Denmark, the United Kingdom, and the Netherlands have been early adopters, integrating direct drive turbines into both onshore repowering projects and large offshore wind farms. With the European Union prioritizing renewable energy under its climate and energy frameworks, demand for advanced turbine technologies that offer higher efficiency and lower lifecycle costs continues to rise. Direct drive systems align well with Europe’s strategic goals of reducing carbon emissions, increasing energy independence, and building resilient power infrastructure.

Download Free Sample Report:https://www.renub.com/request-sample-page.php?gturl=europe-direct-drive-wind-turbine-market-p.php

Key Growth Drivers in the Europe Direct Drive Wind Turbine Market

Expansion of Offshore Wind Installations

Offshore wind power is one of the strongest growth engines for the direct drive wind turbine market in Europe. The region is a global leader in offshore wind capacity, with extensive projects across the North Sea, Baltic Sea, and Atlantic coastline. Direct drive turbines are particularly well suited for offshore environments due to their simplified mechanical design, which reduces failure risks and maintenance requirements in harsh and remote conditions.

As European countries invest heavily in offshore wind to meet carbon neutrality targets, direct drive turbines are increasingly preferred for new installations. Their higher reliability and reduced operational expenditure over the turbine’s lifetime significantly improve project economics. Large-scale offshore developments not only increase demand for high-capacity turbines but also reinforce Europe’s leadership in next-generation wind technology deployment.

Supportive Government Policies and Regulatory Frameworks

Strong policy support at both European Union and national levels plays a critical role in driving market growth. Initiatives such as the EU Green Deal and the “Fit for 55” package place renewable energy at the core of Europe’s energy transition strategy. These frameworks encourage the adoption of efficient and innovative technologies by offering subsidies, favorable financing, and streamlined permitting processes.

National governments further reinforce this momentum through feed-in tariffs, auction mechanisms, and investment incentives aimed at accelerating wind power deployment. Grid modernization and cross-border energy integration initiatives also improve the viability of large wind projects. Collectively, these policies reduce investment risk and create a favorable environment for the adoption of direct drive wind turbines across Europe.

Technological Advancements in Generator Systems

Continuous technological innovation has significantly enhanced the performance and cost-effectiveness of direct drive wind turbines. European manufacturers and research institutions are at the forefront of developing advanced generator technologies, including permanent magnet synchronous generators and electrically excited synchronous generators. These innovations improve energy conversion efficiency, reduce nacelle weight, and enhance turbine reliability.

Digitalization and smart monitoring systems further strengthen the value proposition of direct drive turbines. Predictive maintenance tools, real-time performance monitoring, and advanced control systems allow operators to maximize energy output while minimizing downtime. As manufacturing processes mature and economies of scale improve, the cost gap between direct drive and conventional geared turbines continues to narrow, encouraging broader adoption across Europe.

Challenges in the Europe Direct Drive Wind Turbine Market

High Initial Capital Investment

Despite their long-term benefits, direct drive wind turbines typically involve higher upfront capital costs compared to traditional geared systems. The use of specialized components, advanced materials, and sophisticated manufacturing processes increases initial expenditure. For smaller developers or projects with constrained budgets, particularly in onshore applications, these costs can act as a barrier to adoption.

Although lower maintenance requirements and improved reliability often offset these costs over the turbine’s operational life, the higher initial investment may still influence technology selection. Continued cost reductions, financing support, and policy incentives will be essential to overcome this challenge and expand market penetration.

Dependence on Rare Earth Materials

Many direct drive turbines rely on permanent magnet generators that use rare earth elements such as neodymium and dysprosium. These materials have limited global supply and are subject to price volatility and geopolitical risks. Europe’s reliance on imported rare earth elements raises concerns about supply chain security and long-term scalability.

To address this issue, manufacturers are investing in alternative technologies, such as electrically excited synchronous generators, which eliminate the need for rare earth magnets. While progress is being made, widespread adoption of these alternatives requires further technological refinement and cost optimization.

Europe Electrically Excited Synchronous Generator Market

Electrically excited synchronous generators (EESGs) are gaining traction as a strategic alternative to permanent magnet systems in Europe’s direct drive wind turbine market. EESGs do not rely on rare earth materials, reducing supply chain risks and aligning with Europe’s focus on resource sustainability. These generators offer strong performance, scalability, and suitability for both large onshore and offshore wind farms.

As concerns over material security and environmental impact grow, EESG-based direct drive turbines are expected to see increased adoption. Their compatibility with Europe’s clean energy and industrial resilience goals positions them as a key component of future wind energy development.

Europe Less Than 1 MW Direct Drive Wind Turbine Market

The less than 1 MW segment serves niche applications such as community wind projects, hybrid renewable systems, and rural electrification. In Europe, these smaller direct drive turbines are valued for their quiet operation, ease of maintenance, and strong performance in low-wind conditions. Countries like Italy and Spain support decentralized energy systems through local incentives, encouraging the deployment of compact and efficient direct drive turbines.

Although this segment represents a smaller share of the overall market, it plays an important role in expanding renewable energy access and supporting distributed generation models across Europe.

Europe Onshore Direct Drive Wind Turbine Market

Onshore wind remains a cornerstone of Europe’s renewable energy mix. Direct drive turbines are increasingly being adopted for onshore applications due to their reliability and reduced maintenance needs, particularly in remote or hard-to-access locations. Repowering projects are a major growth driver, as developers replace aging geared turbines with modern direct drive models to improve capacity factors and reduce operational costs.

As land availability becomes more constrained and efficiency requirements increase, direct drive technology offers a compelling solution for maximizing energy output from existing sites.

Europe Offshore Direct Drive Wind Turbine Market

The offshore segment represents the largest and fastest-growing application area for direct drive wind turbines in Europe. Offshore wind farms demand highly reliable systems capable of operating in challenging marine environments. By eliminating the gearbox, direct drive turbines significantly reduce mechanical complexity and maintenance risks, making them ideal for offshore deployment.

Large-scale projects in the North Sea and Baltic Sea, combined with ambitious pan-European climate targets, continue to fuel demand for offshore direct drive turbines. This segment is expected to remain a primary driver of market growth throughout the forecast period.

France Direct Drive Wind Turbine Market

France is strengthening its renewable energy portfolio, with a particular focus on offshore wind development. Government support for local manufacturing and technological innovation aligns well with the advantages of direct drive turbine technology. Both onshore repowering initiatives and new offshore projects are increasingly favoring low-maintenance, high-efficiency turbine designs.

The presence of advanced manufacturing facilities and growing investment in offshore wind infrastructure position France as an attractive market for direct drive turbine suppliers, particularly for large-scale installations.

Germany Direct Drive Wind Turbine Market

Germany is Europe’s largest and most technologically advanced wind energy market. The country активно adopts direct drive turbines for both repowering aging onshore wind farms and expanding offshore capacity. Germany’s strong engineering base and well-developed supply chain support continuous innovation in high-efficiency generators and intelligent turbine systems.

Environmental constraints, land-use limitations, and the need to modernize existing infrastructure further accelerate the shift toward reliable and high-performance direct drive technology in Germany’s wind sector.

United Kingdom Direct Drive Wind Turbine Market

The United Kingdom’s wind energy strategy is heavily focused on offshore development, making it a key market for direct drive wind turbines. With ambitious targets to significantly expand offshore capacity by 2030, demand for advanced, low-maintenance turbine technologies is rising rapidly.

Government incentives, private investment, and local manufacturing initiatives support large-scale deployment of direct drive systems in UK waters. These turbines offer long-term performance benefits and reduced operating costs, aligning well with the country’s offshore wind ambitions.

Russia Direct Drive Wind Turbine Market

Russia’s wind energy market is still at an early stage but shows emerging potential. Recent policy shifts and investments indicate a growing interest in renewable energy, particularly in remote and cold regions where maintenance access is limited. Direct drive turbines offer advantages in such conditions due to their robustness and reduced servicing needs.

However, geopolitical factors, limited domestic manufacturing capacity, and reliance on external technology partners present challenges. Despite these constraints, pilot projects and localized investments suggest gradual growth in the adoption of direct drive wind turbines.

Market Segmentation Analysis

Segmentation by Technology

The market is segmented into electrically excited synchronous generators and permanent magnet synchronous generators. Permanent magnet systems currently dominate due to their high efficiency, while electrically excited systems are gaining momentum as a rare-earth-free alternative.

Segmentation by Capacity

Based on capacity, the market includes less than 1 MW, between 1 MW and 3 MW, and greater than 3 MW turbines. The greater than 3 MW segment leads the market, driven by offshore and large-scale onshore installations.

Segmentation by Deployment Location

Direct drive wind turbines are deployed across onshore and offshore locations, with offshore applications accounting for the largest share due to reliability and lifecycle cost advantages.

Competitive Landscape and Key Players

The Europe direct drive wind turbine market is moderately consolidated, with strong participation from established manufacturers and technology providers. Key players include Siemens Gamesa Renewable Energy SA, ENERCON GMBH, ABB Ltd, VENSYS Energy AG, Leitner AG, Emergya Wind Technologies B.V., ReGen Powertech Pvt. Ltd., Northern Power Systems, and Rockwell Automation Inc. These companies compete through technological innovation, strategic partnerships, and expansion of manufacturing and service capabilities.

Conclusion

The Europe direct drive wind turbine market is set for strong growth through 2033, supported by offshore wind expansion, favorable government policies, and continuous technological advancements. While challenges such as high initial costs and rare earth material dependence remain, innovation and alternative generator technologies are addressing these concerns. As Europe accelerates its transition to a low-carbon energy future, direct drive wind turbines will play an increasingly vital role in delivering reliable, efficient, and sustainable wind power across the region.